what is a credit score?

|

A credit score is a tool lenders use to help analyze information in your credit report to help them make lending decisions. Your score is determined by comparing the information in your credit report to how millions of customers performed in repaying debt over time. In comparing this, the lender is able to determine the relative risk that you may become delinquent on your account or default on a loan.

It is a 3 digit number that typically ranges from 300 to 850, those that are based on the standard FICO scoring. |

|

what is a credit report?

A credit report is a historical report that compiles your complete financial history. A numerical rating is then determined from this historical data and that is your credit score.

The numerical rating is done by a credit reporting agency, Equifax, Experian, and Transunion. When you receive your credit score, you will receive three numbers, one from each agency.

The numerical rating is done by a credit reporting agency, Equifax, Experian, and Transunion. When you receive your credit score, you will receive three numbers, one from each agency.

building credit

Credit cards are the easiest way to build credit but also the quickest way to ruin credit.

The best option for establishing credit is to apply for a secured credit card. This credit card is backed by a cash deposit that you put upfront, that amount is your credit line and is kept by the company as collateral in case you fail to pay you bill. The deposit will be returned when you close the account. This is best option because it is a safe way to establish good credit. These are to be used until you can establish a good credit score and are able to get an unsecured credit card. Choose a secured credit card with low fees and one that reports to all 3 credit reporting agencies.

The most important thing to remember in building your credit is to pay your bills in full on time every single month. Even being a little late and/or not paying your bills in full can greatly decrease your credit score.

The best option for establishing credit is to apply for a secured credit card. This credit card is backed by a cash deposit that you put upfront, that amount is your credit line and is kept by the company as collateral in case you fail to pay you bill. The deposit will be returned when you close the account. This is best option because it is a safe way to establish good credit. These are to be used until you can establish a good credit score and are able to get an unsecured credit card. Choose a secured credit card with low fees and one that reports to all 3 credit reporting agencies.

The most important thing to remember in building your credit is to pay your bills in full on time every single month. Even being a little late and/or not paying your bills in full can greatly decrease your credit score.

what is included in your credit score?

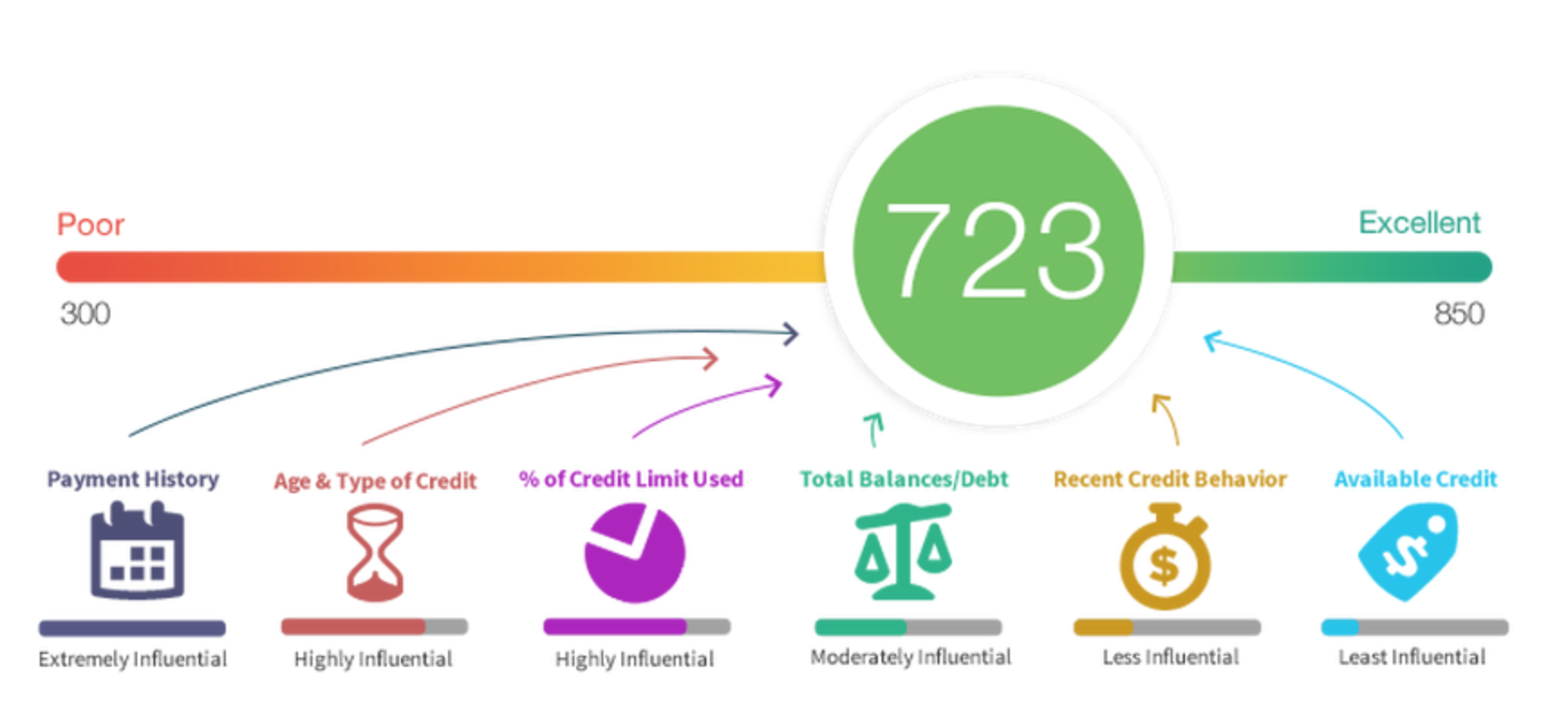

Payment History is the most influential part of your credit score. This includes your record of on-time payments and late payments. Paying your bills on time consistently is what influences the payment history part of your credit score. This typically counts for 35% of your credit score.

Length of Credit History (Age & Type of Credit) is pretty self explanatory. The longer you have had credit, the better because the more evidence available to lenders to determine your creditworthiness . Issuers are more likely to lend to someone who has had perfect credit for 5 years than to someone who has also had perfect credit but only for 2 years.

Credit Utilization/Utilization Rate is the percent of credit available to one person that is being used, in the diagram below it it referred to as "% of Credit Limit Used." The higher the ratio, the lower your score will typically be. The reason for this is because the lenders consider someone who uses more of their available credit to be a riskier borrower. It is calculated by taking the total amount outstanding balances divided by the sum of all the limits on your credit card(s). The preferred percentage is 35% or less for most issuers.

However it can be difficult to only use 35% of your credit card limit, you can try to raise your credit card limit which will allow you to spend more but still staying under 35% of your total limit. It is also possible to simply use another credit card when you have reached 35% of your limit on one card. But keep in mind you should not raise your credit limit or get another credit card if you cannot be financially responsible with one credit card!

Amount Owed (Total Balances/Debt) is the amount you currently owe to lenders. In your FICO score, this category can also be broken down into other subcomponents including, the amount owed to lenders,

Length of Credit History (Age & Type of Credit) is pretty self explanatory. The longer you have had credit, the better because the more evidence available to lenders to determine your creditworthiness . Issuers are more likely to lend to someone who has had perfect credit for 5 years than to someone who has also had perfect credit but only for 2 years.

Credit Utilization/Utilization Rate is the percent of credit available to one person that is being used, in the diagram below it it referred to as "% of Credit Limit Used." The higher the ratio, the lower your score will typically be. The reason for this is because the lenders consider someone who uses more of their available credit to be a riskier borrower. It is calculated by taking the total amount outstanding balances divided by the sum of all the limits on your credit card(s). The preferred percentage is 35% or less for most issuers.

However it can be difficult to only use 35% of your credit card limit, you can try to raise your credit card limit which will allow you to spend more but still staying under 35% of your total limit. It is also possible to simply use another credit card when you have reached 35% of your limit on one card. But keep in mind you should not raise your credit limit or get another credit card if you cannot be financially responsible with one credit card!

Amount Owed (Total Balances/Debt) is the amount you currently owe to lenders. In your FICO score, this category can also be broken down into other subcomponents including, the amount owed to lenders,

what is included in your credit report?

Credit reporting will differ slightly depending on which company you are receiving your information from, however, they all contain the same categories of information.

Identifying information like your social security number, employer, address, name, all the basics that are used to identify who you are (these are not considered when considering your credit score)

Trade Lines, also known as Tradelines, are your credit accounts. Tradelines include credit cards, mortgages, loans, etc. They contain the name of the creditor or lender from which the money is being borrowed, the amount of money borrowed, the date the account was opened and other account milestones (like maximum amount ever owed, date of first delinquency, if any, and any defaults).

The payment status is the most important part of the tradelines. This section tells whether or not the money is being paid back on time, or how late they are being paid back. Higher credit scores typically have multiple tradelines all of which have been open for about 2 years, and, most importantly, that the credit line has not been exhausted and payments have not been missed.

Credit Inquiries are when you have applied for a loan or another line of credit. These are requests from a legitimate organization that has asked for a copy of your credit report. They are either classified as soft or hard inquiries. Soft inquiries are when someone who is not a prospective lender is looking at your credit (i.e. checking your own credit, inquiries by businesses with whom you already have an account, or sometimes businesses will inquire for promotional uses).

Hard inquiries are when potential lenders access your credit because you have applied for credit with them, you must authorize these types of inquiries. Only hard inquiries have an effect on your FICO score. Typically one hard inquiry will not affect your credit score, but if lenders see that you have multiple inquiries especially in a short span of time, they may consider you a high-risk customer.

Credit History is the complete payment history. Closed accounts, that have been paid, will always remain on your credit report, typically unpaid accounts will remain on your credit report for 7 years.

Public Records and Collection Amounts which are if any of your unpaid debts have been sent to collection agencies and any other public information. Even something as little as $10 can appear in this section and it is not good to ever have anything, so make sure you are keeping track of your money and making smart financial decisions. Other public information includes bankruptcies, foreclosures, and lawsuits. Also included are tax liens (defined in the keywords section) which are notices attached by courts that block the sale of something until the debt is paid off.

Identifying information like your social security number, employer, address, name, all the basics that are used to identify who you are (these are not considered when considering your credit score)

Trade Lines, also known as Tradelines, are your credit accounts. Tradelines include credit cards, mortgages, loans, etc. They contain the name of the creditor or lender from which the money is being borrowed, the amount of money borrowed, the date the account was opened and other account milestones (like maximum amount ever owed, date of first delinquency, if any, and any defaults).

The payment status is the most important part of the tradelines. This section tells whether or not the money is being paid back on time, or how late they are being paid back. Higher credit scores typically have multiple tradelines all of which have been open for about 2 years, and, most importantly, that the credit line has not been exhausted and payments have not been missed.

Credit Inquiries are when you have applied for a loan or another line of credit. These are requests from a legitimate organization that has asked for a copy of your credit report. They are either classified as soft or hard inquiries. Soft inquiries are when someone who is not a prospective lender is looking at your credit (i.e. checking your own credit, inquiries by businesses with whom you already have an account, or sometimes businesses will inquire for promotional uses).

Hard inquiries are when potential lenders access your credit because you have applied for credit with them, you must authorize these types of inquiries. Only hard inquiries have an effect on your FICO score. Typically one hard inquiry will not affect your credit score, but if lenders see that you have multiple inquiries especially in a short span of time, they may consider you a high-risk customer.

Credit History is the complete payment history. Closed accounts, that have been paid, will always remain on your credit report, typically unpaid accounts will remain on your credit report for 7 years.

Public Records and Collection Amounts which are if any of your unpaid debts have been sent to collection agencies and any other public information. Even something as little as $10 can appear in this section and it is not good to ever have anything, so make sure you are keeping track of your money and making smart financial decisions. Other public information includes bankruptcies, foreclosures, and lawsuits. Also included are tax liens (defined in the keywords section) which are notices attached by courts that block the sale of something until the debt is paid off.

why should you care?

Your credit score plays a vital role in your financial journey. Your credit score is checked when you are applying for a mortgage, a loan, a car, etc and they greatly impact the outcome of whether or not you can get that mortgage, loan or car. Lenders want to lend their money to someone who is going pay them back and that's why they look at your credit score. Although there are companies and places that will give you the loan if you do not have a good credit score, they come with sky high interest rates and fees. So high that if you are having trouble paying back the money you already owe, it's not a smart decision to continue to borrow even more money.

Having a low credit score can affect whether or not you are approved for car insurance, a rental property, a cell phone and even a job. In most of these cases, your credit score is being checked to determine how responsible you are. If you cannot be responsible with your money, more likely than not it will be assumed you cannot be responsible in most other areas too.

Overlooking the importance of your credit score is very damaging to your financial health, which is why it is so important to practice good financial habits. Missing one payment is not the end of the world, it is not good, but if you make the effort to fix your mistake and you never do it again, you can recover. A good credit score is a major key to financial success.

Having a low credit score can affect whether or not you are approved for car insurance, a rental property, a cell phone and even a job. In most of these cases, your credit score is being checked to determine how responsible you are. If you cannot be responsible with your money, more likely than not it will be assumed you cannot be responsible in most other areas too.

Overlooking the importance of your credit score is very damaging to your financial health, which is why it is so important to practice good financial habits. Missing one payment is not the end of the world, it is not good, but if you make the effort to fix your mistake and you never do it again, you can recover. A good credit score is a major key to financial success.

key words

DELINQUENT - if you delinquent on your account payment refers to any account that is past due, usually an account is not considered delinquent until at least 30 days have passed the due date in which the credit card holder has not made a minimum payment. After 30 days, will result in a lower credit score.

DEFAULTING ON A LOAN - defaulting on a loan means you are unable to pay back the money owed (usually after 9 months) then you are considered to have defaulted on a loan. The lender can then take legal action if he or she wishes, and usually the unpaid debt will be sent to a collection agency. A debt collection is one of the worst types of credit report accounts.

A collection agency is a third party agency hired by the lenders who collect money from people who have defaulted on a loan.

FICO - FICO is a data analytics company that focuses on reporting credit scores by measuring consumer risk. It has now become a fixture of US consumer lending

LIENS - is the right to hold possession of something from another person until their debt is paid off

DEFAULTING ON A LOAN - defaulting on a loan means you are unable to pay back the money owed (usually after 9 months) then you are considered to have defaulted on a loan. The lender can then take legal action if he or she wishes, and usually the unpaid debt will be sent to a collection agency. A debt collection is one of the worst types of credit report accounts.

A collection agency is a third party agency hired by the lenders who collect money from people who have defaulted on a loan.

FICO - FICO is a data analytics company that focuses on reporting credit scores by measuring consumer risk. It has now become a fixture of US consumer lending

LIENS - is the right to hold possession of something from another person until their debt is paid off